Drivers of our investment philosophy

Our convictions for a meaningful investment product:

- A return source must be clearly understandable, logically consistent, and measurable

An investment concept should transparently define how returns are generated, which risks are taken, and which underlying drivers are responsible for performance. Ideally, the return sources are fully quantifiable. - Only systematic success is truly reproducible

The causal link between investment decision and investment outcome must be traceable. Performance that is not generated through a clearly defined set of rules and processes is unlikely to be consistently replicable over time. - Forecast independence is more robust and closer to market reality than attempts at market timing

Forecasts rely on a range of assumptions about correlations and causal relationships, often derived from historical data. In practice, however, these relationships are rarely stable and can change abruptly. As a result, strategies based on forecasting and timing tend to be less reliable. - Continuity and risk reduction are essential to avoid drawdowns or enable their rapid recovery

A stable return profile is more effectively achieved when an investment concept is designed to manage drawdowns both proactively and reactively. This must be embedded in the process rather than decided after losses occur, with the objective of optimising the risk-return profile. - Complexity should be reduced by excluding uncompensated risks (exclusive use of listed options, hedging of currency exposures)

Investment concepts are often over-engineered in an attempt to perform across as many scenarios as possible. This typically leads to lower transparency and unintended interactions within the portfolio. - Liquidity ensures flexibility

Unless the strategy is explicitly designed to harvest illiquidity premia, investment concepts should focus on the most liquid market segments, where responsiveness is highest and execution costs are lowest.

Case Study: The Volatility Risk Premium

There are several explanations for the origin of the volatility risk premium. A particularly well-documented aspect is the historically elevated pricing of put options, often referred to as the “overpriced puts puzzle,” which cannot be fully explained by standard option pricing models. This phenomenon has been extensively studied in academic literature (e.g. in “Why are Put Options so Expensive?” by Oleg Bondarenko, published in The Quarterly Journal of Finance in 2014).

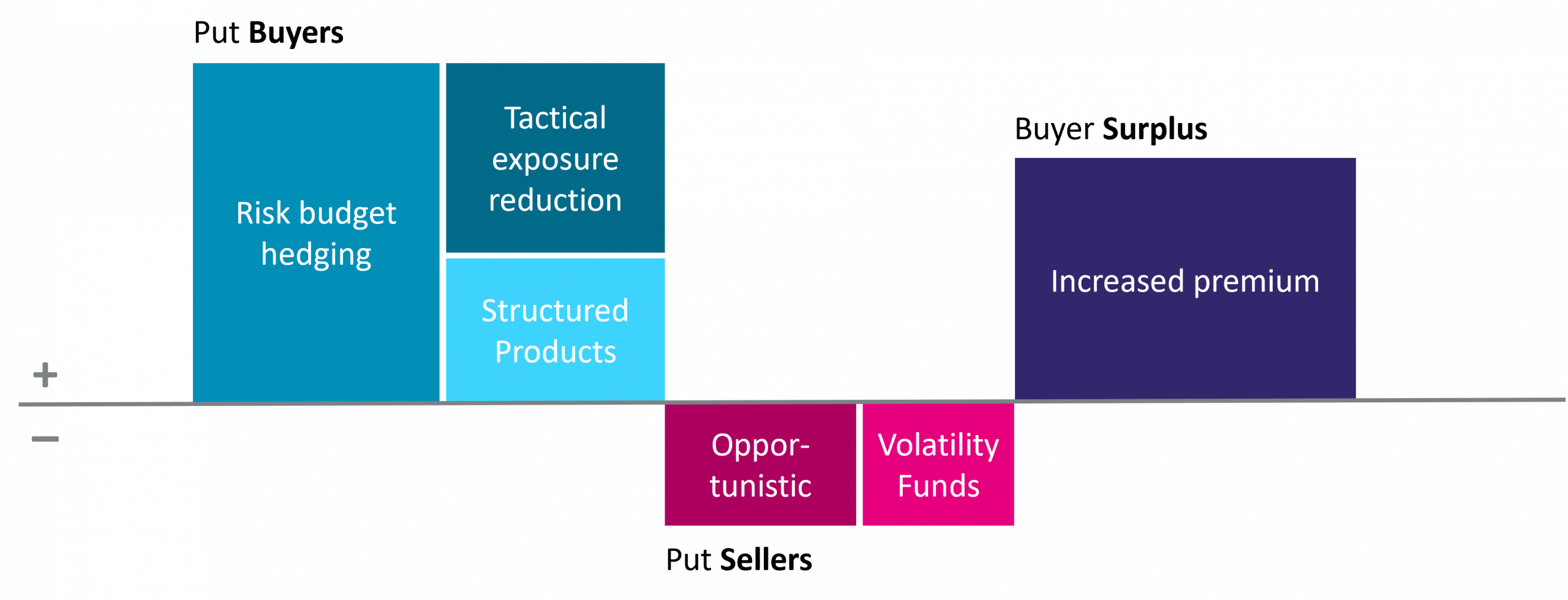

In our view, the most intuitive explanation, even though it is not formally captured by a pricing model, is a persistent imbalance between buyers (long) and sellers (short) of options, in particular put options. This imbalance is driven by structural and long-lasting demand for downside protection, which results in a sustained buyer surplus and consequently in systematically elevated put prices.

Empureon Volatility One

The fund aims to systematically and risk-consciously capture the volatility risk premium in the US equity market.

Fund Unit Class Overview Volatility One Fund

Empureon US Equity

The fund aims to generate systematic and risk-controlled outperformance relative to the S&P 500.

Fund Unit Class Overview US Equity Fund

Empureon Europe Equity

The fund aims to generate systematic and risk-controlled outperformance relative to the STOXX Europe 600.

To achieve this, the fund broadly replicates the STOXX Europe 600 Index through single-name equities and, where appropriate, futures, and complements this exposure with a premium strategy.

The investment concept of the premium strategy consists of three core components. The first component involves the systematic sale of exchange-traded index put options, which serves as the primary source of premium income. To limit downside risk from this position, further out-of-the-money index put options are purchased. This second component uses the same number of contracts and the same expiration dates as the short put positions.

The third component is a tail hedge designed to provide additional protection against extreme market environments and, in certain scenarios, to benefit from them. Strike selection and position sizing are determined in a fully rule-based manner and adjusted depending on the prevailing market environment.

Additional systematic features, including diversified rolling of positions, predefined profit-taking rules, and allocation across multiple expiries, further reduce risk and enhance the risk-return profile.